Sep 21, 2023

Balanced budgets and free trade really do help nations to prosper.

The International Monetary Fund—what is that again? News coverage of such events as the G-20 conferences periodically reminds us that activists like to protest this institution. Casual observers may not know much else about it. The IMF was founded at American behest in 1944, an era of the gold standard and fixed exchange rates, as a currency stabilization fund. It still exists today, presumably as such, in our era of floating exchange rates. As Ronald Reagan quipped, the only hard evidence we have of eternal life is a government program.

Jamie Martin’s The Meddlers is a history of the origins of the IMF as can be discovered in the economic operations of the novel international institutions of the post-World War I period. The ill-fated League of Nations, the Treaty of Versailles organization established without American participation in 1920, and the Bank of International Settlements (BIS) founded in 1930, are the primary examples. This highly detailed book contends that such institutions transmitted pre-1914 western imperial economic practices into the world of fledgling nation-states that emerged out of the general crisis of World War I. In turn, the IMF called on this precedent after World War II and itself became a colonialist stand-in for the great powers.

Greece, Austria, China, and other new or reconstituted states found themselves, in the 1920s and 1930s, subject to economic diktats from the League and allied organizations that resembled the commands that Britain and France, and to a degree the United States, had put on their imperial spaces in the nineteenth century. Strictures of “conditional loans”—a central term in this book—insisted upon by great-power bankers backing League/BIS credits made these bankers the arbiters of domestic monetary and fiscal practices in the countries getting the money. Thereby the League and the BIS went about “reproducing” colonialism—another of this book’s idioms—and conveyed imperial habits to the IMF. The IMF would specialize in conditional loans to new sovereign nations in its activities in the decolonization period after World War II.

“Austerity” is a cliché of political-economic intellectual discourse, with negative connotations.

Imperialism changed clothes, to use the Thomas Carlyle expression, via the institutions of “global economic governance” (another term from The Meddlers) over the course of the twentieth century. Formal became informal imperialism. As Antonio Gramsci lamented, capitalist hegemony is hard to stop. It has a particular talent for taking on attractive guises, if necessary, of internationalism and cooperation while the old one-way streets of metropolitan control of the periphery keep apace.

The concept of “sovereignty” is the leitmotif of The Meddlers. It was the core-of-identity that both new countries and fading powers (eventually including Britain) had to cede away, in the economic policy realm, in the face of colonialism-reproducing institutions on the order of the League and then the IMF. Economic policy sovereignty is, however, a terribly difficult concept to define—a problem that dogs the historical interpretations that this book offers.

An example that Martin treats at length was a League loan to Austria as this new state confronted a 200-fold price inflation in the early 1920s. “During 1920-1922,” Martin writes, “as Austria’s rescue was debated by a range of public and private actors beyond its borders, most assumed that the stabilization of the krone required the Austrian government to relinquish full autonomy over its domestic fiscal and monetary policies.” Austria got the loan in October 1922, complete with determinations that it had to cut the government payroll and make its currency all but convertible in gold. As for the fledgling country’s experience under the loan conditions, “it took more than two years of austerity and the sacking of nearly 100,000 government workers, in the face of fierce Social Democratic resistance, for Austria to be declared stabilized.”

“Austerity” is a cliché of political-economic intellectual discourse, with negative connotations. As for denotation, any plausible meaning has to include tight money, high tax rates, and minimal government spending. The main plank of the loan conditionality in 1922 was for the Austrian central bank to dispense with the bonds of its own government and issue currency on the margin exclusively on the basis of gold, foreign assets, and high-quality commercial paper, preferably the former two of these options.

Martin could have been clearer in this regard, specifying that Austria had to make the choice of basing its domestic money on its central bank’s ownership of outside money, namely foreign assets and specifically gold, and perhaps citing economics Nobelist Thomas Sargent’s notable paper on this matter from the 1980s. As Sargent detailed, in the fall of 1922, Austria saw, on initiating the plans of the League-brokered loan, the real domestic money supply of its economy rise by sixfold and stay at an elevated level for the duration. The huge noninflationary Austrian monetary expansion of late 1922 was the opposite of austerity.

Martin is dismissive of the gold standard. He likes to describe it as a form of “fetters.” This is an academic tic. Popularized by Barry Eichengreen’s 1992 book Golden Fetters: The Gold Standard and the Great Depression, the term “fetters” has become, in economic historical scholarship, the shadow of any consideration of the gold standard. It is a simple way of side-stepping any serious argument about the gold standard, ignoring among other things the fact that a transition to largely gold-defined money can greatly increase demand for currency (as in the Austrian case of 1922).

Martin laments that “the new or reformed independent central banks of the postwar were almost without exception established in countries that did not, in practice, enjoy full economic sovereignty,” listing countries from Central Europe, the Balkans, Latin America, South Asia, and Africa. “Would a powerful government, like that of Britain,” he asks, “allow questions about the pound to be put in foreign hands in an institution that it would not be able to control directly?”

The proposition that countries, even the greatest hegemons, control their currencies is a difficult one to sustain. Exchange rate markets, let alone the gold standard of bygone times, express this point baldly. No sovereign controls the price of a currency until markets (inclusive of the participation of many a foreign institution) make that price a fact. “Questions about the pound” or the dollar, or any traded currency are posed every instant in the now $7 trillion-per-day exchange rate markets.

Independent monetary policy, as Robert Triffin taught in the 1960s, is an impossibility given fixed exchange rates and global economic integration. Such conditions were the norm before 1914. The whole world’s experience prior to World War I (through a booming industrial revolution) was that there was little sovereign control over money. “Monetary policy” did not exist as a term on any scale until the 1920s.

When income tax rates were already high, and primed to change, who knew what currencies were likely to be worth after all the responsive capital flows? Bankers making loans had to hedge.

When it comes to fiscal policy, Martin does offer some interesting discussions. It is fascinating to learn more about the new international banking and policy bureaucrats that rose in the interwar period, and valuable to understand how these types raised the suspicions of those leaning toward radical political movements. But once again, the major issues remain elusive. The League as well as the BIS insisted upon certain tax, spending, and regulatory policies in sovereign countries getting loans. Yet of course this happened. If a country’s currency is to maintain its rate of exchange to that of the country from which the loan comes (and the currency in which the loan must be repaid), then the fiscal profiles of both countries have to be nearly identical, or at least unchanging.

To be fair to Martin, this old economic verity (of Ricardo’s) is underappreciated today in the discipline of economics. Given that prices of goods, and of factors of production, are the same the world over if there is a minimum of trade (a Paul Samuelson proof), the existence of a tax in one country but not another will alter the exchange rate. High tax rates in one place make the currency less valuable than that in the other place (assuming that government spending is not unusually enlightened), because the tax differential falls on factors of production that have the same price the world over. Capital will flow toward the country with lower final after-tax prices, appreciating the exchange rate of the low-tax country. League or BIS loans insisting on a specific fiscal policy profile indicated that the creditors wanted to be paid back in a medium as valuable as that which they supplied. Conditional loans respectful of this reality were only natural.

Martin misses an opportunity to address points of this nature in a passage concerning French travails in the mid-1920s. As Martin writes:

In France, there was also widespread criticism of the private nature of the BIS, which opponents claimed would allow foreign bankers to override the policies of the French government and provide a Trojan Horse for US financial imperialism in Europe. One important precedent for such worries was the response of the Banque de France to the financial instability faced by the Third Republic in 1925-1926, when the bank had refused to use its gold reserves to support the franc, leading to a fissure between the bank and the government and accusations that the former had effectively starved out the left coalition in power.

Martin does not tell us that from 1924-1926, France increased its income tax such that the top progressive rate was suddenly the highest by a sight among the major powers at levels over 70 percent. Capital powered out of France to where it could get better return, depreciating the franc. Fiscal policy was not so sovereign after all. Pick one the market disapproves of, and the currency will fail.

Martin is remiss in declining to address the comprehensive emergence of income taxation after World War I. The effects on exchange rates and capital allocations were incalculable. Prior to 1914, the gold standard and fixed exchange rates had a predicate. Major countries had a modest fiscal profile, mild if any income taxation, and small government. Alterations to the terms of trade in the form of differential fiscal policies essentially did not exist. It was the perfect time for fixed exchange rates, anchored in gold. The economy responded with epic growth, delivering mass prosperity.

From the 1920s onwards, the income tax changed everything. When income tax rates were already high, and primed to change, who knew what currencies were likely to be worth after all the responsive capital flows? Bankers making loans had to hedge. If their efforts to manage the situation sometimes took the form of “meddling”—new-era bureaucrats shuttling around insisting upon terms—this was a symptom at a degree of removal from the cause.

Niall Ferguson has observed that neo-Marxian scholarship is heretical in seeing superstructures as determining events over base. For over a century now, the central concern of western Marxism has been to explain how capitalism persists because its cultural forms enable it to overwhelm its material contradictions. The Meddlers, in similar fashion, refrains from examining issues of economic structure in favor of arguing, by way of extensive archival and secondary literature research, that novel international financial bureaucracies were the mechanism by which the cultural forms of capitalism reproduced themselves over the centuries to drive history.

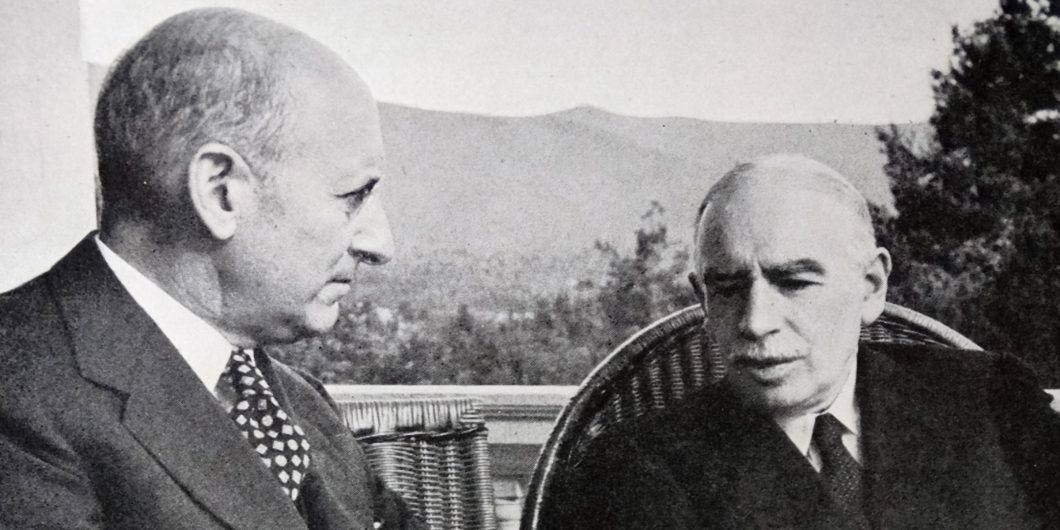

The last chapter of The Meddlers, on the IMF, is a sympathetic recounting of British attempts, led by John Maynard Keynes, to stave off the American plan to return everyone to fixed rates, or even to gold. Keynes knew that the fiscal policy Britain had its heart set on in the 1940s—industry nationalization—would decimate the pound in the markets, as in fact happened. Martin once again keeps distance from such formal issues and avails himself of language such as “the rigidities of gold,” “onerous forms of conditionality,” and “neoliberals.” Whatever the origins of the IMF, neo-colonialism is not the interpretive framework one needs to understand the peculiar economic policy history of the interwar period. Classical economics is perfectly illuminating.

Balanced budgets and free trade really do help nations to prosper.

Richard Spady's account of economic growth reminds us of the tensions between domestic growth and development abroad, but the path forward isn't clear.

Understanding the narratives of political economy can improve communication, and help us to appreciate subtle truths about our political moment.