Apr 12, 2019

Without Trump in play, the pre-existing party system will snap back into place with issues and coalitions little altered.

Oren Cass wants to reverse the decline of American manufacturing and our ever-increasing dependency on imports, with good reason. Loss of manufacturing jobs imperils the economic standing of tens of millions of Americans; technological innovation atrophies when it is separated from production; loss of manufacturing undermines America’s strategic position; and, finally, no country can sell assets indefinitely to support a perpetual trade deficit. I am Cass’s comrade-in-arms: In 2020 I wrote the cover essay for a collection of papers on re-shoring industry published by his organization, The American Compass.

The question is, what changes in economic policy will improve our circumstances? For every complex problem there is an answer that is simple, clear, and wrong, H. L. Mencken said, and tariffs fit that description. Politicians like tariffs because they produce revenue, a desirable characteristic when our federal budget deficit exceeds 7% of GDP, a level unheard of except in wartime or severe recession. The alternatives—including tax incentives for manufacturing investment, selective subsidies for industry, federal support for R&D, training for engineers and skilled workers, and improved infrastructure—all cost money that Congress is now reluctant to spend.

There are several problems with tariffs. They raise the price of imported goods, giving domestic manufacturers an advantage. In some cases, they are indispensable. The US imposes a 27.5% tariff on imports of cars from China. Without this, China would crush America’s auto industry. Whether this is due to Beijing’s subsidies to automakers or due to enormous economies of scale in the highly automated plants of the world’s largest producer is beside the point. No American manufacturer can compete with the $11,000 sticker price of BYD’s Seagull subcompact. America can’t afford to lose its auto industry, and there is a strong case for protection. Our special 25% tariff on Chinese imports, moreover, may not be enough, because Chinese car companies are building production plants around the world. President Reagan, a free marketeer by conviction, used outright import quotas to prevent Japanese automakers from crushing the American industry, forcing the Japanese giants to build plants in the United States.

We will never catch up to China in raw numbers of STEM personnel. But our track record of innovation is unique in the world.

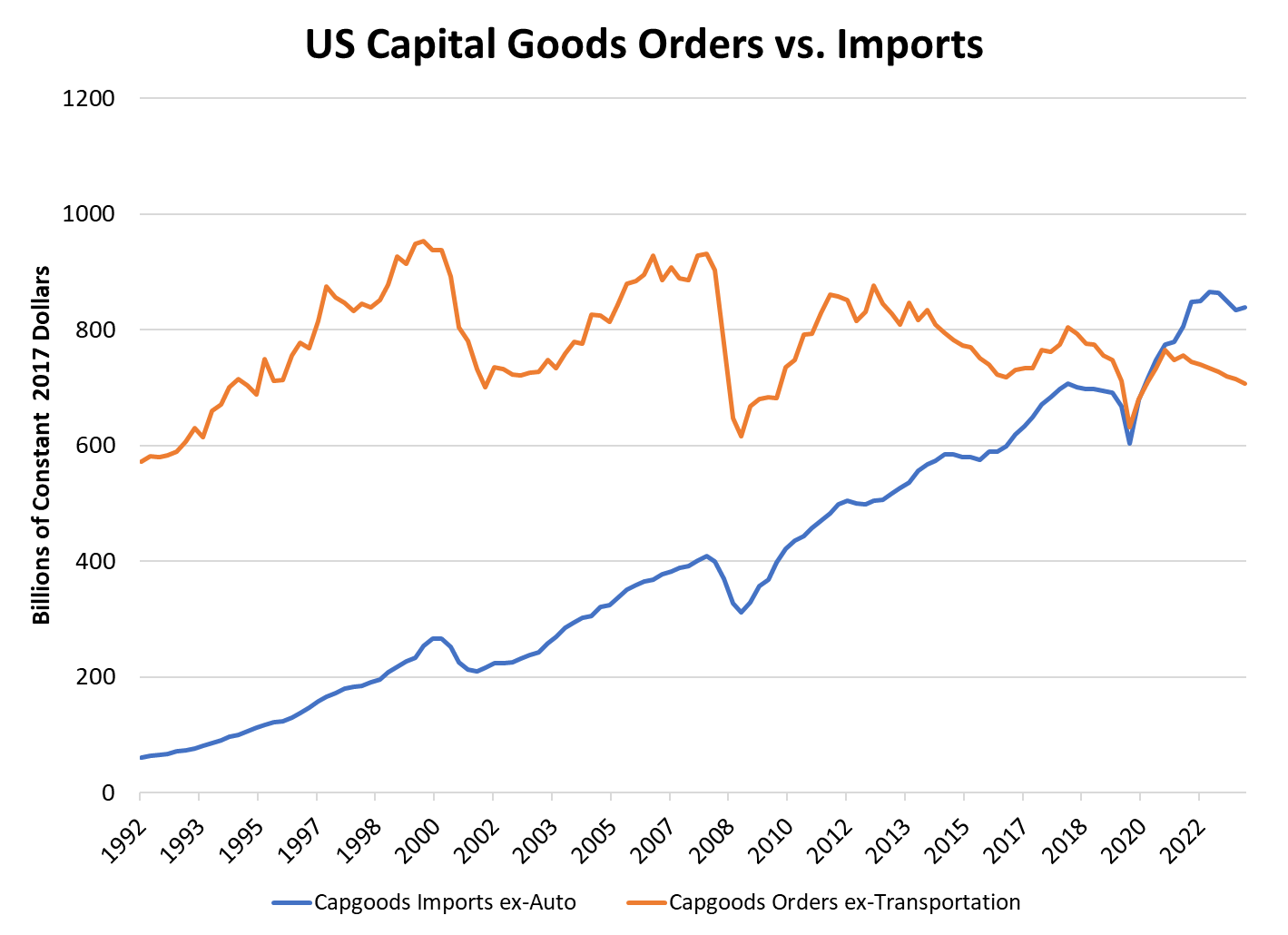

In other cases, tariffs may be harmful. To correct the trade deficit, we have to produce more at home, and to produce more we first have to invest more. For the first time in our history, though, we import more capital goods—the goods that make other goods—than we produce at home. The chart below compares imports of capital goods (excluding automotive) to domestic orders for nondefense capital goods excluding transportation. (Both series are shown in constant 2017 dollars at annual rates.) We crossed the line during the COVID-19 epidemic, and now import more capital goods than we produce at home.

As a matter of arithmetic, that means we have to import more in the short term to invest in industries that, in the long term, will reduce our dependence on imports. American industry depends on foreign components—especially Chinese components—for thousands of items that we no longer produce at home, starting with circuit boards, but including capacitors, switches, and a myriad of electronic parts. That’s true even in the defense industry. Reported by the Financial Times on June 19, 2023:

Greg Hayes, chief executive of Raytheon, said the company had “several thousand suppliers in China and decoupling . . . is impossible.” “We can de-risk but not decouple,” Hayes told the Financial Times in an interview, adding that he believed this to be the case “for everybody.” “Think about the $500bn of trade that goes from China to the US every year. More than 95 percent of rare earth materials or metals come from, or are processed in, China. There is no alternative,” said Hayes. “If we had to pull out of China, it would take us many many years to re-establish that capability either domestically or in other friendly countries.”

It’s one thing to make Chinese autos more expensive for US consumers to keep our auto industry alive. But would it help us to make capital goods more expensive for US manufacturers? I’m quite sure that it would hurt us.

Our persistent trade deficit has many causes, but the most important of these is the reluctance of Americans to invest in capital-intensive industries. After the 2000–01 recession, the smart money figured out that we could produce expensive software and let Asia make the hardware—first Japan, then South Korea and Taiwan, and then China. The marginal cost of selling a download of a computer program from a website is zero; not so the marginal cost of fabricating another computer chip or building a plasma screen.

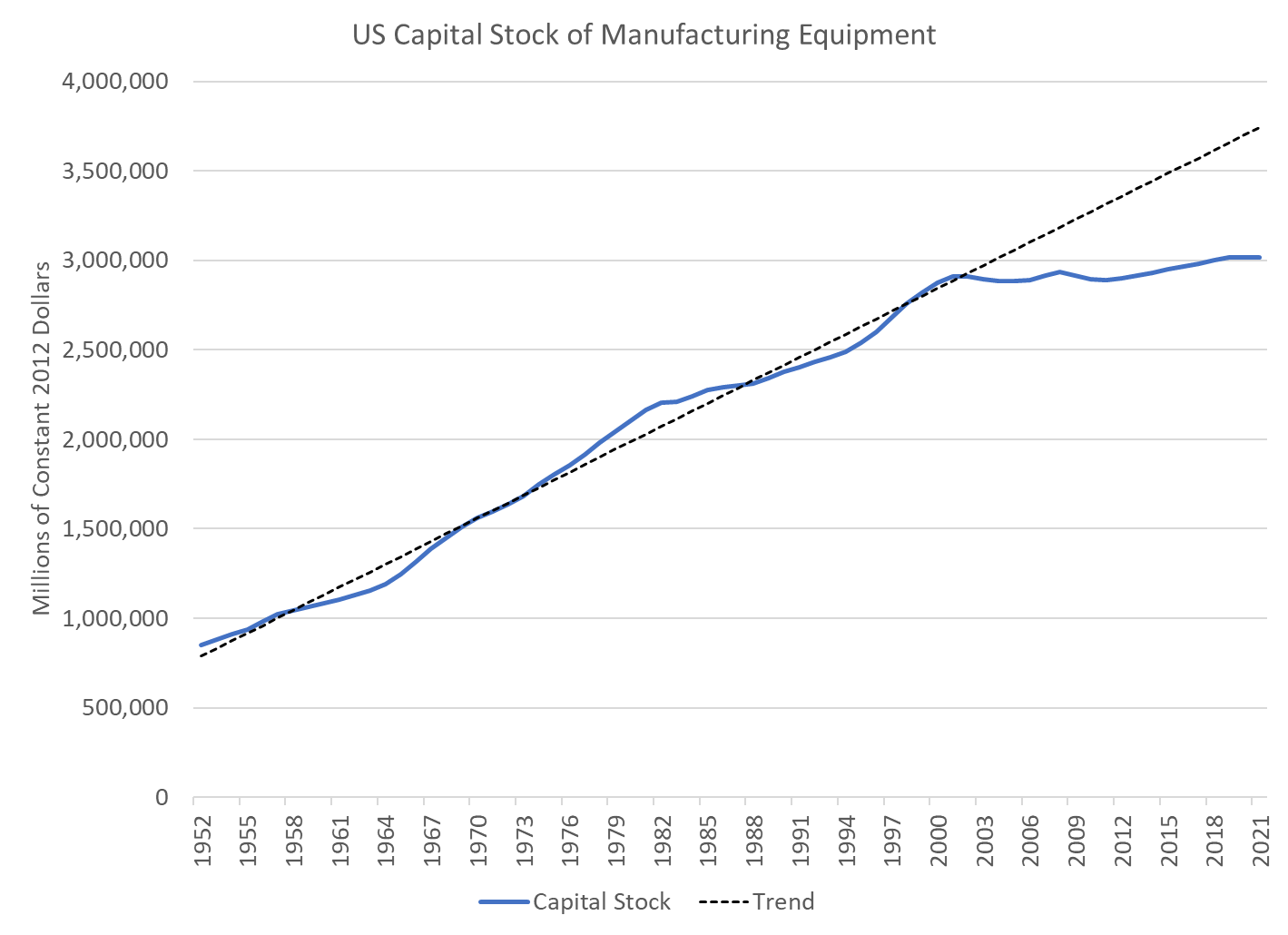

Our capital stock of manufacturing equipment stopped growing in 2001, according to Federal Reserve estimates. To get back to our long-term trend growth in manufacturing capital stock, US manufacturers would have to spend about $1 trillion for new equipment, nearly five years’ worth of purchases at current rates.

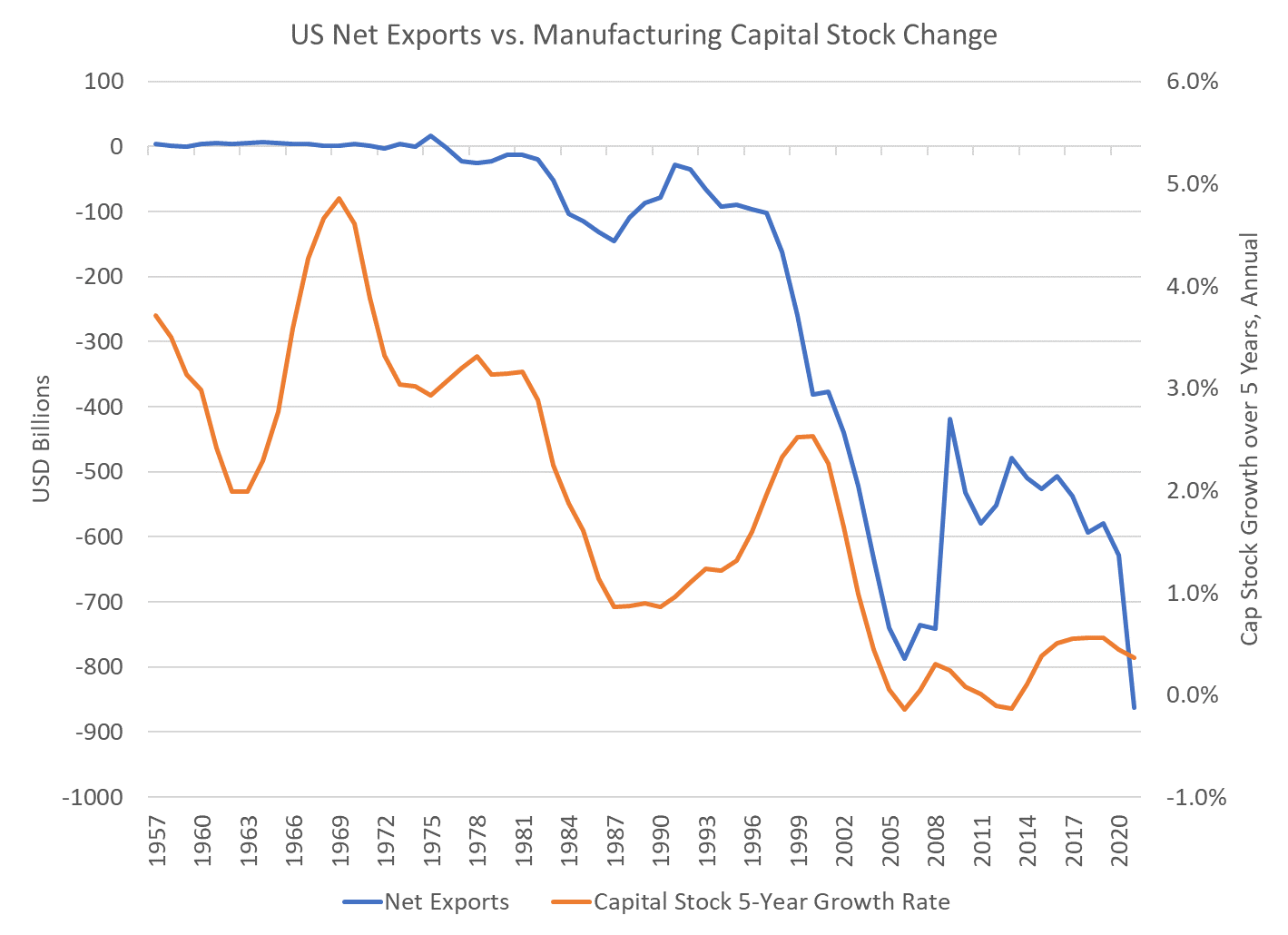

There’s a clear correspondence between our trade deficit and the slowing growth rate of manufacturing capital stock. The growth rate of capital stock slowed well before the trade deficit ballooned during the 2000s.

The Trump tariffs haven’t kept Chinese goods out of the United States. China’s exports to the US surged to a post-COVID seasonally-adjusted peak of $52 billion a month in March 2022 from $38 billion in August 2019, when the tariffs were announced. China exported a seasonally adjusted $36 billion to the US in October 2023, according to US customs data. Chinese data show an increase from $34 billion in August 2019 to $42 billion in October 2023. The Chinese data probably are more accurate, according to a Federal Reserve study, because they include exports routed via third countries. More to the point, America’s trade deficit in goods and services was $48 billion in August 2019 (or $576 billion annualized). In October 2023 it rose to $64 billion, or $768 billion annualized.

According to recent studies by IMF economists, the World Bank, the Peterson Institute, Bank for International Settlements (BIS) researchers, and others, tariffs haven’t made the US less dependent on Chinese supply chains. The Chinese shipped semi-finished goods and components to third countries for final assembly and re-export to the United States. As the BIS wrote: “Firms from other jurisdictions have interposed themselves in the supply chains from China to the United States. The identity of the firms that have interposed themselves in this way can be gleaned from the fact that firms from the Asia-Pacific region account for a greater portion of suppliers to US customers than in December 2021, as well as accounting for a greater portion of the customers of Chinese suppliers.” The World Bank economists put it this way: “US imports from China are being replaced with imports from large developing countries with revealed comparative advantage in a product. Countries replacing China tend to be deeply integrated into China’s supply chains and are experiencing faster import growth from China, especially in strategic industries. Put differently, to displace China on the export side, countries must embrace China’s supply chains.”

In April 2023, Asia Times released my study of US trade dependencies under the title, “The Great Re-Shoring Charade.” We came to the same conclusion: The United States imported less from China only because it imported more from countries dependent on Chinese semi-finished goods, components, and capital goods.

What will it take to persuade US manufacturers to invest in expensive, capital-intensive plants? There are several issues, including

In a 2023 monograph for the Claremont Institute, I outlined what policies needed to change to restore American manufacturing.

Tariffs have a role to play in reviving manufacturing, but that role should be narrowly defined and industry-specific, as in the case of autos. There is no way to climb out of the hole we have dug for ourselves without spending money—on tax relief for manufacturing investment, on infrastructure, and in rare cases such as semiconductors, on subsidies.

As noted, American manufacturers would need to spend roughly an additional $1 trillion on capital equipment to get our capital stock of manufacturing equipment back to trend. If the capital/labor ratio in manufacturing were to remain constant, we would have to hire 3.25 million manufacturing workers. As noted, we can’t find 600,000 workers for the jobs already advertised. We can’t reverse a quarter-century of decline overnight. That means the American manufacturing industry will have to pick its spots, rather than attempt to replace imports across the board.

The term that economists use for picking one’s spots is “comparative advantage.” We do the things we’re best at and import things that would cost too much to make at home. There’s no reason not to import steel from Brazil or Canada, or circuit boards from China, or textiles from Indonesia. Those are low-margin businesses. There are industries we should subsidize, for example, telecommunications equipment. We rely on two Scandinavian equipment makers, Nokia and Ericsson, for our broadband infrastructure. Between them, they spend about $9 billion a year on R&D, compared to $25 billion for Huawei. Huawei and its smaller Chinese rival ZTE together control 45% of the world telecom equipment market, with an overwhelming market share in the Global South. We had an opportunity in 2017 to compete with Huawei and create a national champion. We bungled it, and as a result, we are behind not only in 5G network rollout, but a generation behind China in the application of high-speed broadband to factory automation.

Using the resources of the Defense Department, we should concentrate on flexible manufacturing. As the venture capitalist Henry Kressel, who headed RCA Labs at its creative peak, wrote in Asia Times:

Forget the old image of factories where workers are standing on an assembly line bolting parts together. We are talking of plants run with sophisticated information technology (IT) by highly trained technicians. Robots do the work.

Built around modular units, such plants can be expanded as needed, or partially not used, without impacting the operating modules. The production flexibility is enabled by tooling and software changes to move products quickly from development to production, thus closely integrating manufacturing with product development, marketing, and sales.

Flexible high-tech manufacturing relies on the creative application of IT through the use of massive timely data and artificial intelligence, robotics, sensor deployment, and ubiquitous communications to link the factors bearing on manufacturing. Such plants with suitable interlinked sensors are well suited for a high level of in-process quality control and documentation.

This is critical for national security as well as economic reasons. The US imported US$33 billion in capital goods from China for electricity generation and distribution in 2022, items that are no longer manufactured in the US. Substituting domestic production for these items would entail long lead times and exorbitant costs, industrial officials say. In the event of a full-scale trade war, a Chinese ban on critical components could cripple basic US infrastructure.

A shift to flexible manufacturing, though, requires broadband infrastructure. China’s Huawei claims that it has 10,000 industrial customers for private 5G networks, which transmit high volumes of data for AI-assisted manufacturing through wireless networks. I know of only three in the United States (Ford Motors, General Motors, and John Deere). We need a national 5G network, and that will require subsidies.

In 2019, a Huawei executive told me: “We don’t understand why the Americans didn’t have Cisco buy Ericsson and create a competitor.” Some months later, then-presidential economic adviser Larry Kudlow pitched the idea to Cisco CEO Chuck Robbins. As the Wall Street Journal reported, “Mr. Robbins ‘didn’t want the US to fall behind’ … but the company, which makes computer networking gear, was unwilling to invest in a less profitable business like Nokia or Ericsson without some sort of financial incentives.” As a matter of general principle, subsidies to specific industries are a dangerous proposition, but there are exceptions. Broadband is one of them.

Oren Cass and I are shooting at the same varmints, but I think he is misdirecting his ire at the theory of comparative advantage. It’s worth reading carefully what Prof. Justin Yifu Lin writes in a new book on China’s economic future. A University of Chicago PhD, Prof. Lin was chief economist of the World Bank and now is a senior advisor to China’s State Council. He cites the term “comparative advantage” nine times in the cited essay. For example:

According to the new structural economics I advocate, a vital principle for economic development is for nations to make good use of their comparative advantages. To bring comparative advantage into full play, the economy needs a vibrant market to mobilize entrepreneurs’ enthusiasm and allocate resources well. …

Given that developed countries began developing their economies at the start of the Industrial Revolution—with capital accumulated over hundreds of years—their per capita financial and material capital is much greater than China’s, giving them comparative advantages in traditional capital-intensive industries.

For the new economy with short R&D cycles and human capital as the main input, the importance of financial capital is relatively small. In this domain, China and developed countries are on the same starting line, but China has advantages in human capital compared with many developed countries. …

China has a population of 1.4 billion people and therefore a potentially large number of such intelligent individuals and, as such, it has an advantage in this new economy, the main input of which is human capital.

China’s tertiary education rate when Deng Xiaoping began his market reforms in 1979 was just 3%. Now it’s 63%, about the same as Germany’s. It graduates 1.2 million engineers and computer scientists each year, more than the rest of the world combined. It proposes to deploy its breadth and depth of human capital to lead in high-tech industries.

What is America’s comparative advantage? We will never catch up to China in raw numbers of STEM personnel. But our track record of innovation is unique in the world. The United States invented the entirety of the digital age, not only because the Defense Advanced Research Projects Agency subsidized research, but because the great corporate laboratories encouraged the creative few to pursue novel ideas that led to hitherto unimagined technologies that created entire new industries. Public-private partnerships put the burden of fundamental research on the federal government, but left the risk of commercialization to private capital.

China has shown that given a well-defined objective—for example, fabricating the high-end chips that it can no longer buy from the United States—it will surprise the world. China picks its targets—solar cells, electric vehicles, and now legacy chips—and takes them out systematically. The United States still has the opportunity to lead the world in technologies that haven’t yet been invented and new industries that no one has imagined. That is our comparative advantage.

Without Trump in play, the pre-existing party system will snap back into place with issues and coalitions little altered.

William Howard Taft’s reflections on the old convention system remind us that things don’t have to be this way.